Do You Need Water And Sewer Line Insurance? Everything You Need To Know

If so, you're not alone. Many homeowners find themselves asking this question when faced with the possibility of unexpected plumbing disasters. Water and sewer lines are essential components of your home's infrastructure, but they are also prone to wear and tear over time. A single burst pipe or sewer line collapse can lead to thousands of dollars in repair costs, leaving you financially strained. This is where water and sewer line insurance comes into play, offering peace of mind and financial protection against such unforeseen events. While standard homeowners' insurance policies typically cover damage caused by water leaks inside the home, they often exclude issues related to underground water and sewer lines. These lines are subject to a variety of risks, including tree root intrusion, ground shifting, and aging infrastructure. Repairs can be complex, requiring excavation and specialized labor, which can quickly escalate costs. Understanding the role of water and sewer line insurance and whether it's a worthwhile investment is crucial for every homeowner. This article delves deep into the topic, exploring its benefits, costs, and alternatives, so you can make an informed decision. Whether you're a new homeowner or someone who has lived in the same house for decades, understanding the nuances of water and sewer line insurance is essential. The goal of this article is to provide you with a comprehensive overview of this type of coverage, helping you determine whether it's a necessary addition to your insurance portfolio. By the end, you'll have a clear understanding of what water and sewer line insurance entails, its pros and cons, and whether it aligns with your specific needs and budget.

Table of Contents

- What is Water and Sewer Line Insurance?

- Water and Sewer Line Insurance: Do I Need This?

- What Does Water and Sewer Line Insurance Cover?

- How Much Does Water and Sewer Line Insurance Cost?

- Is Water and Sewer Line Insurance Worth the Investment?

- Are There Alternatives to Water and Sewer Line Insurance?

- What Are the Common Misconceptions About Water and Sewer Line Insurance?

- Frequently Asked Questions About Water and Sewer Line Insurance

What is Water and Sewer Line Insurance?

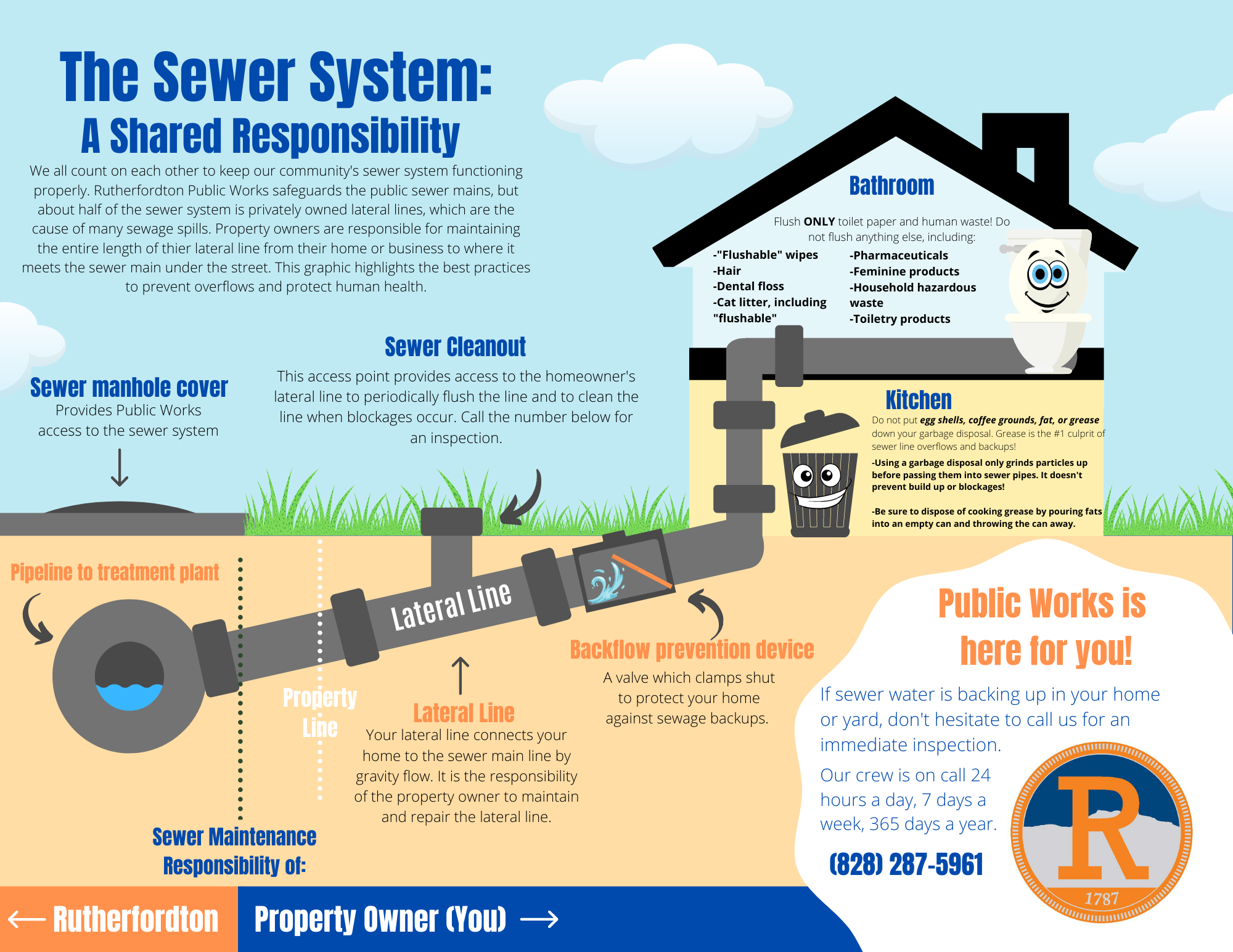

Water and sewer line insurance is a specialized type of coverage designed to protect homeowners from the financial burden of repairing or replacing damaged underground water and sewer lines. Unlike standard homeowners' insurance, which typically excludes these components, water and sewer line insurance specifically addresses issues that arise from the external infrastructure of your home. This type of policy can be purchased as a standalone product or as an add-on to an existing homeowners' insurance plan. The primary purpose of water and sewer line insurance is to cover the costs associated with repairing or replacing damaged lines. These costs can include excavation, labor, materials, and even landscaping restoration if your yard is disrupted during repairs. For example, if a tree root infiltrates your sewer line, causing a blockage, this insurance would cover the expenses of removing the root, repairing the line, and restoring your yard to its original condition. Similarly, if a water line bursts due to freezing temperatures, the policy would cover the necessary repairs. Understanding the scope of this insurance is crucial. It is not a catch-all solution for every plumbing issue but rather a targeted coverage for external lines. Homeowners should be aware that internal plumbing problems, such as leaks inside the house or issues with appliances like water heaters, are typically not covered. Additionally, some policies may have exclusions for pre-existing conditions or damage caused by neglect. Therefore, it's essential to read the fine print and ensure that the coverage aligns with your specific needs and risks.

Water and Sewer Line Insurance: Do I Need This?

Determining whether you need water and sewer line insurance requires a careful evaluation of several factors. One of the most significant considerations is the age of your home. Older homes, particularly those built before the 1970s, often have water and sewer lines made from materials like clay or cast iron, which are more prone to corrosion and failure. If your home falls into this category, investing in water and sewer line insurance may be a prudent decision. Another critical factor is the location of your property. Homes situated in areas with extreme weather conditions, such as freezing temperatures or frequent flooding, are at a higher risk of water and sewer line damage. Additionally, if your property is surrounded by large trees, the roots can infiltrate and damage underground lines over time. In such cases, the likelihood of needing repairs increases, making insurance a valuable safeguard. Similarly, homes in regions with older municipal infrastructure may face higher risks due to external factors beyond the homeowner's control. Your financial situation also plays a role in deciding whether water and sewer line insurance is necessary. While the monthly premium for this coverage is relatively affordable, ranging from $5 to $15, the cost of repairs without insurance can be staggering. For instance, repairing a sewer line can cost anywhere from $3,000 to $20,000, depending on the extent of the damage and the complexity of the repair. If an unexpected repair bill would strain your finances, water and sewer line insurance can provide peace of mind and financial protection.

Read also:Scarlett Johansson Height And Weight A Comprehensive Guide To Her Life And Career

What Are the Signs That You Might Need Water and Sewer Line Insurance?

Several warning signs indicate that you may benefit from water and sewer line insurance. One of the most obvious is a history of plumbing issues in your neighborhood. If your neighbors have experienced frequent water line breaks or sewer backups, it's likely that your property is at risk as well. Additionally, if you notice slow drainage, foul odors, or wet spots in your yard, these could be early indicators of underlying problems with your lines.

How Does Your Home's Infrastructure Affect the Need for Insurance?

The material and condition of your water and sewer lines are key determinants of whether insurance is necessary. Homes with outdated materials like clay, cast iron, or galvanized steel pipes are more susceptible to damage. On the other hand, properties with modern PVC or HDPE pipes may have a lower risk. Conducting a professional inspection of your lines can help you assess their condition and make an informed decision about insurance.

What Does Water and Sewer Line Insurance Cover?

Water and sewer line insurance provides coverage for a wide range of issues that can affect your underground infrastructure. The most common problems include leaks, cracks, and blockages caused by external factors such as tree roots, ground shifting, or freezing temperatures. For example, if a tree root infiltrates your sewer line, causing a blockage, the insurance would cover the costs of removing the root, repairing the line, and restoring your yard. Similarly, if a water line bursts due to freezing temperatures, the policy would cover the necessary repairs. In addition to covering the direct costs of repairs, many policies also include additional benefits. These may include coverage for excavation, which can be a significant expense, as well as landscaping restoration. Some policies even offer reimbursement for temporary accommodations if your home becomes uninhabitable during repairs. However, it's important to note that water and sewer line insurance typically excludes issues caused by neglect or pre-existing conditions. For instance, if a line fails due to a lack of routine maintenance, the policy may not provide coverage.

What Specific Scenarios Are Typically Covered?

Most policies cover scenarios such as line breaks caused by natural disasters, accidental damage during construction, and deterioration due to normal wear and tear. However, coverage may vary depending on the provider, so it's essential to review the terms carefully. Some policies may also offer optional add-ons, such as coverage for municipal lines or additional living expenses.

How Much Does Water and Sewer Line Insurance Cost?

The cost of water and sewer line insurance can vary significantly based on several factors, including the age and location of your home, the length of your water and sewer lines, and the coverage limits you choose. On average, homeowners can expect to pay between $5 and $15 per month for this type of insurance. While this may seem like a small expense, the financial protection it provides can be invaluable in the event of a major repair. To put this into perspective, consider the potential costs of repairing or replacing a damaged water or sewer line. A typical repair can range from $1,000 to $5,000, while more extensive issues, such as a complete sewer line replacement, can cost upwards of $20,000. When weighed against these potential expenses, the monthly premium for water and sewer line insurance becomes a relatively small price to pay for peace of mind. Additionally, some providers offer discounts for bundling this coverage with other insurance policies, making it even more affordable.

What Factors Influence the Cost of Water and Sewer Line Insurance?

Several factors can influence the cost of your policy, including the material and condition of your lines, the risk of natural disasters in your area, and the provider's underwriting criteria. Homes with older or deteriorating infrastructure may face higher premiums, while properties in low-risk areas may qualify for lower rates. It's also worth noting that some policies offer customizable coverage limits, allowing you to tailor the policy to your specific needs and budget.

Read also:What Are Examples A Comprehensive Guide To Understanding And Using Examples Effectively

Is Water and Sewer Line Insurance Worth the Investment?

When evaluating whether water and sewer line insurance is worth the investment, it's essential to weigh the potential benefits against the costs. For many homeowners, the peace of mind that comes with knowing they are protected from costly repairs is invaluable. Consider this: a single sewer line collapse can result in repair costs exceeding $10,000. If you live in an area with older infrastructure or are concerned about the condition of your lines, the relatively low monthly premium for this insurance can provide significant financial protection. However, not everyone may find this coverage necessary. For instance, if your home is relatively new and equipped with modern, durable pipes, the likelihood of experiencing a major issue may be lower. In such cases, the cost of the insurance may outweigh the potential benefits. Additionally, some homeowners may prefer to set aside funds in an emergency savings account to cover unexpected repairs rather than paying for insurance. Ultimately, the decision depends on your individual circumstances, risk tolerance, and financial priorities.

Are There Alternatives to Water and Sewer Line Insurance?

If you're hesitant about purchasing water and sewer line insurance, there are alternative options to consider. One common approach is to set aside funds in a dedicated savings account specifically for home repairs. By regularly contributing to this account, you can build a financial cushion to cover unexpected plumbing issues. However, this method requires discipline and may not provide immediate relief in the event of a major repair. Another alternative is to invest in preventative maintenance. Regular inspections and timely repairs can help identify and address minor issues before they escalate into costly problems. For example, having your sewer lines professionally cleaned every few years can prevent blockages caused by tree roots. Similarly, insulating your water lines during the winter months can reduce the risk of freezing and bursting. While these measures can mitigate risks, they do not offer the same level of financial protection as insurance.

What Are the Common Misconceptions About Water and Sewer Line Insurance?

Many homeowners harbor misconceptions about water and sewer line insurance, which can lead to uninformed decisions. One common myth is that standard homeowners' insurance covers all plumbing-related issues. In reality, most policies exclude damage to underground water and sewer lines, leaving homeowners financially vulnerable. Another misconception is that water and sewer line insurance is prohibitively expensive. While the cost varies, the monthly premium is often quite affordable, especially when compared to the potential costs of repairs. Some people also believe that this type of insurance is unnecessary if their home is relatively new. While newer homes may have a lower risk of line failures, they are not immune to issues such as tree root intrusion or ground shifting. Additionally, municipal infrastructure problems can impact even the most modern properties. By understanding these misconceptions, homeowners can make more informed decisions about whether water and sewer line insurance is right for them.

Frequently Asked Questions About Water and Sewer Line Insurance

Does Homeowners' Insurance Cover Water and Sewer Line Repairs?

No, standard homeowners' insurance typically does not cover repairs to underground water and sewer lines. These issues are considered external and are usually excluded from basic policies. Water and sewer line insurance is specifically designed to fill this gap in coverage.

Can I Add Water and Sewer Line Coverage to My Existing Policy?

Yes, many insurance providers offer water and sewer line coverage as an add-on to existing homeowners' insurance policies. This can be a convenient and cost-effective way to enhance your coverage without purchasing a standalone policy.

What Should I Look for in a Water and Sewer Line Insurance Policy?

When shopping for a policy, look for coverage that includes excavation, landscaping restoration, and optional add-ons like municipal line coverage. Be sure to review the exclusions and limitations to ensure the policy meets your specific needs

Fortnite Default Face: A Complete Guide To Its Popularity And Impact

How To Check And Manage Your Vanilla Gift Card .com Balance Effectively

Wynonna Judd Height: A Comprehensive Look At Her Life, Career, And Legacy

Do You Need Water & Sewer Line Insurance? Western Rooter & Plumbing

My Home Sewer Line Rutherfordton, NC